Matt McKenna

Underwriting Manager

Key Takeaways

Underwriting Manager

The past decade has been a booming era for mergers and acquisitions (M&As). Many company leaders continue to see deal activity and opportunities abound, making M&As a vital growth driver. Yet, executing a smooth transition is tricky (and rare). Knowing what insurance policies you need during an M&A can change a company’s outcome significantly. That said, here’s a multi-angled look at several M&A points to consider.

Mergers & Acquisitions Trends

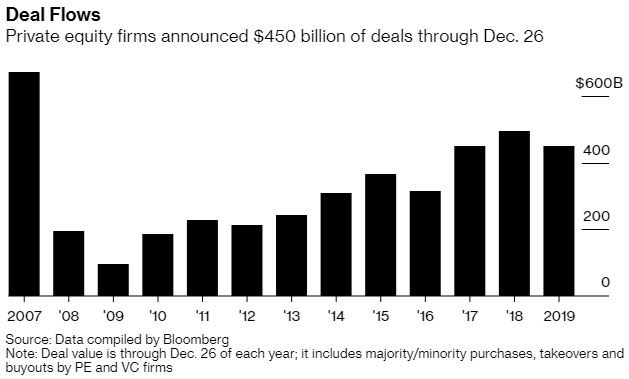

Since 2013, US companies have announced transitions worth in aggregate over $10 trillion. It comes as no surprise that this impressive figure is record-setting. Specific sectors, regions, and deal types continue to welcome fresh opportunities to support expansion.

According to Deloitte, US companies held $1.55 trillion in cash (or “dry powder”) at the close of 2019. Although this number was down slightly from 2018, many companies intended to use most of that cash for M&A activity. Of course, the COVID-19 pandemic and impending US elections play crucial roles in most business decisions nowadays.

When the world experienced a massive virus-induced shutdown earlier this year, global M&As were paused. Most companies struggled to stay afloat and had no choice but to walk away from takeover deals. For example, Xerox abandoned its $35 billion bid of the rival printing company, HP. Its leadership stated that focusing on the pandemic’s impact on its operations was a top priority.

Knowing that nothing lasts forever, the pandemic will end. However, the astounding 8-year M&A run might end soon, as well. Geopolitical and macroeconomics factors will undoubtedly impact the outlook. But no one knows if these dynamics will shove the M&A market out of the black — only time will tell.

M&A Considerations

No matter if the M&A market’s glorious sun is setting, deals will continue to close, and businesses will keep joining forces. Some experts have a unique insight into the situation. Take Jason Langan, partner at Deloitte & Touche LLP, for example, and his M&A eye-opener:

“If the economy slows, let alone dips into a recession, companies aren’t going to ignore M&A — they are just going to be even more deliberate in the deals they look to do. That might mean more divestitures, an effort to raise cash or shed units that just aren’t performing. Some also are going to be strategic about using a downturn to buy assets more cheaply; this is especially true on the PEI side, which has large cash reserves. Typically M&A doesn’t disappear in a downturn — but some strategic imperatives shift.”

Jason Langan, partner, M&A Services, Deloitte & Touche LLP

Despite the potential headwind that this market might face, a strategy will play a vital role in how the future plays out. Naturally, grandeur plans haven’t been absent entirely from the M&A market. However, Langan indicates that deliberation will stand on the frontlines more than ever before — which brings us to the idea of insurance alignment in M&As.

What Is Insurance Alignment?

Before we delve into a few essential pre-M&A questions, let’s talk about coverage. Aligning insurance plans is merely reviewing each company’s current insurance policies, matching or mirroring them as needed. What is this vital? Without adequate coverage on both sides, gaps and liabilities abound. Plenty of claims have sizzled out because either party didn’t cover the loss.

Furthermore, these out-of-pocket expenses burn holes in company pockets. Knowing how the buyer’s and the seller’s insurance will respond to a control change is crucial. Who assumes liability? This knowledge will prevent gaps, and it will also secure run-off coverage. Once you’ve aligned your insurance coverage, it’s time to start thinking in terms of intricate details.

Are Your Leaders Protected?

For starters, are your management team’s decisions and actions covered by adequate directors and officers (D&O) insurance? The professional responsibilities of directors and officers can be summed up in three categories, which include the duties of:

- Diligence: Leaders complete duties in good faith, with the company’s best interests in mind.

- Loyalty: Leaders remain loyal to the company, undistracted by any conflicts of interest.

- Obedience: Leaders conduct company business within the boundaries of the law.

These three duties are undoubtedly put to the test during a merger or acquisition. If someone accuses a director or officer of failing in one of their duties, massive D&O lawsuits typically follow. D&O insurance protects company leaders from personal liability caused by a professional decision or action. Plus, carriers can usually customize D&O coverage to your company’s needs and modify them during M&As.

Are Agreements Backed Up?

Post-acquisition litigation is what happens after the dust has settled from an M&A, and one party accuses the other party of breaching one of the many agreements. The incurred damages are often messy, and the legal defense fees are costly. What’s more, many businesses are taken aback after realizing that their general liability insurance doesn’t cover such claims.

Only representation and warranties (R&W) insurance works specifically to reduce the vulnerabilities that come with M&As. This coverage is informally known as “transactional risk insurance” and often works in tandem with the company’s D&O policy. It’s must-have coverage when buying or selling a company.

If substantial M&A lawsuits occur, months and even years could pass until the parties reach some agreement. Representation and warranties insurance help sellers and buyers avoid this costly legal situation by:

- Indemnifying the buyer according to the agreement terms and conditions with the seller up to the policy limit.

- Providing capital for defense costs and judgments or settlements against the seller.

Do Your Workers’ Compensation Policies Align?

Aligning workers’ compensation insurance is one of the most frequently forgotten aspects of M&As. As a result, many company leaders face a rude awakening regarding their new premium. After all, workers’ compensation premiums rely on several factors, such as industry, years in operation, claim history, employee pool size, and state-established codes and rates.

For example, suppose you recently merged with a business that has shoddy safety practices. Their experience modification rate (X-Mod) — the figure summing up workers’ compensation history — is incredibly high. It’s unlikely that your premiums will remain the same after the merge as it was before since underwriters will now consider both X-Mods in their process.

Again, this can be a rude awakening to company leadership. A better approach is to thoroughly examine both companies’ condition and prepare to accept any additional exposures. Getting to the root cause of a high X-Mod would be a sound strategy, as well.

Who Will Cover Liabilities?

The liability landscape can change drastically, depending on the sale type. In some sales, such as stock sales, the buyer acquires the seller’s assets and liabilities. Naturally, any liabilities after the sale fall on the buyer’s general liability policy.

In other sales, such as asset sales, the buyer only acquires the assets of the seller. The buyer deliberately leaves the seller’s liabilities on the deal table — the buyer didn’t want those. Therefore, the seller’s liability policy continues to cover for any losses or damages. Eventually, the seller will shutter. It makes sense that when the doors close for good, the insurance policies end, as well.

However, problems surface when claims pop up after the seller has ceased operations. To avoid these issues, the seller and buyer should consider other policy options to cover bodily injury and property damage. Talking with a seasoned insurance professional will provide you with tailored options to fit your specific M&A needs, no matter where your loopholes lie.

Understanding the details of what coverage your company needs can be a confusing process. Founder Shield specializes in knowing the risks your industry faces to make sure you have adequate protection. Feel free to reach out to us, and we’ll walk you through the process of finding the right policy for you.

Want to know more about M&A insurance? Talk to us! You can contact us at info@foundershield.com or create an account here to get started on a quote.