Carl Niedbala

Managing Partner; COO & Co-Founder

Key Takeaways

Managing Partner; COO & Co-Founder

Do you have employees? It’s a simple enough question that most founders can answer with a one-word response — yes or no. Do you think your employees would ever file a lawsuit against you? Although this question is slightly more unearthing than the first one, it’s still valid. Employee-related claims have been on the rise for several years. As a result, employee practices liability insurance (EPLI or EPL insurance) has served as a lifesaver for many young companies. But when is the best time to purchase EPLI coverage?

In this post, we look at several situations that prompt founders to bump “buy EPL insurance” to the top of their to-do list. Let’s dive in!

What Is EPLI Coverage?

Before we jump right into why a startup should purchase EPLI coverage, let’s go over the basics of this policy. EPL insurance helps to cover companies for employee lawsuits that arise from their employment conduct practices, such as:

- Breach of employment contract

- Discrimination

- Wrongful termination

- Failure to employ or promote

- Negligent evaluation

- Sexual harassment

- Wrongful discipline

- Mismanagement of employee benefit plans

- Wrongful infliction of emotional distress

Naturally, having employees creates an array of vulnerabilities for founders to manage. What’s more, we live in a litigious society. Many people don’t think twice about filing a lawsuit against another individual or company, no matter the ramifications. Additionally, government regulations funnel employees into litigation more times than not.

Some recent trends in employment claims include issues about wage lawsuits, the #metoo movement, and medical marijuana. Naturally, with so many potential problems, EPLI is a go-to resource for quick-thinking founders.

For more information, check out some employment practices liability coverage examples to understand better how this insurance can protect your business.

We frequently see this type of coverage coupled with directors and officers (D&O) insurance, especially in startups. This double whammy offers secure protection for rapidly growing businesses.

When Do Startups Usually Get EPLI Coverage?

Unfortunately, plenty of startups opt for EPLI coverage after it’s too late — but the “afterthought” approach isn’t the only way to go.

When They Experience a Claim

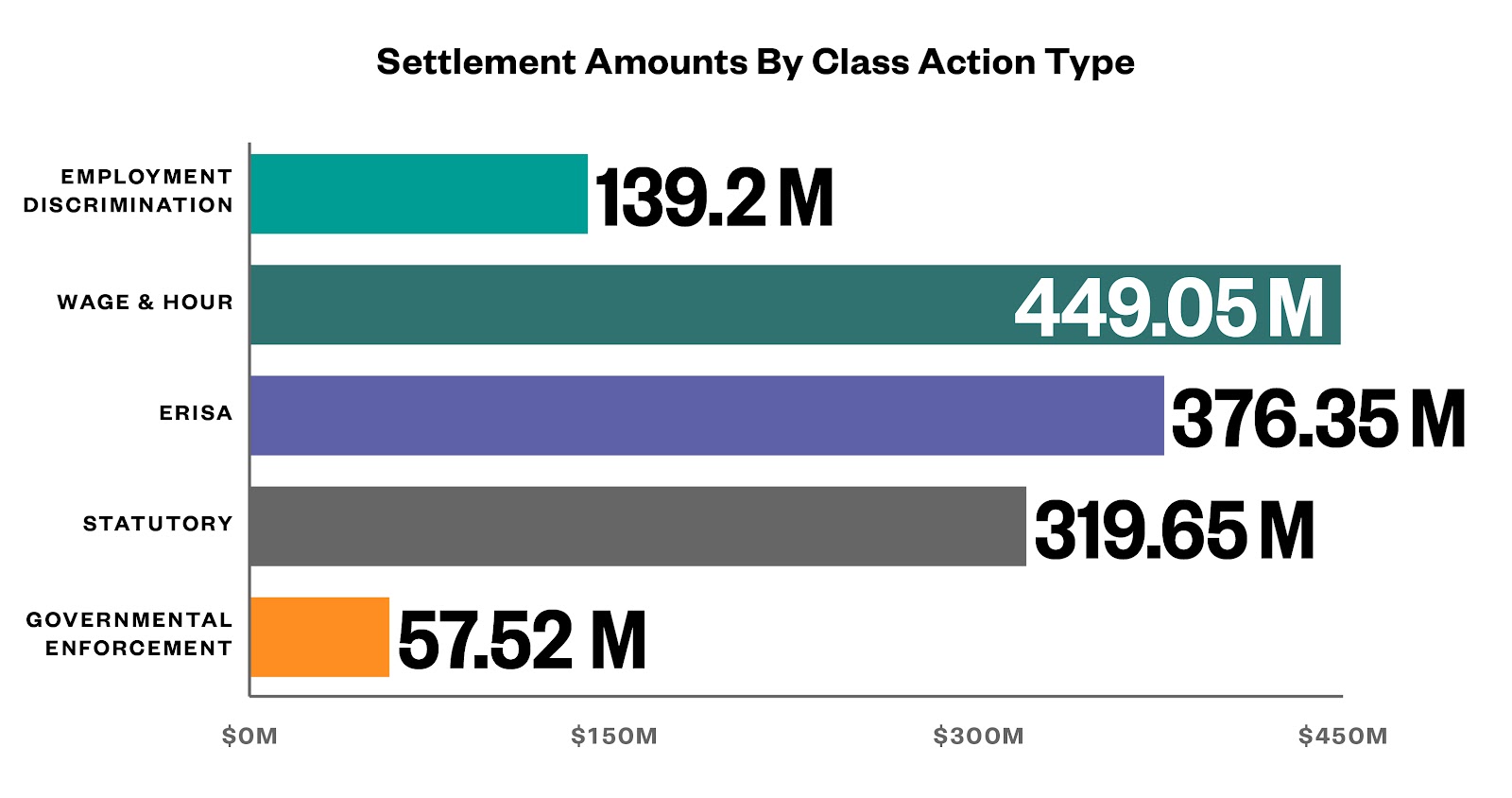

Although many founders have impressive foresight, sometimes, an unexpected lawsuit is what lights the fire to get more coverage. After dealing with a messy claim, startups grapple for EPL insurance faster than the speed of light.

Check out the graph below, displaying settlement amounts. The figures are shocking and motivate founders to safeguard their business before it’s too late.

When They Expect Rapid Transformation

A professional growth spurt doesn’t typically happen out of the blue. Instead, it takes strategic planning and execution that often involves product placement, content marketing, advertising, etc. An excellent idea is for founders to review their plans for growth before any of this happens.

For example, are you expecting a wave of hiring or firing in the next 12-18 months? New team members typically signify growth and also open the door for employee-related issues. However, downsizing your team, for any reason, holds similar risks.

If you anticipate a period of rapid expansion or significant transformation, it would be best to cover your bases first. Especially if it involves fresh faces on your workforce team or your company climate is going to be vastly different than when you founded the company.

Consider this nugget of “scaling up” wisdom from Colin Angle, CEO of iRobot, “Culture is the secret ingredient to scaling up a company,” he said. “To scale hiring, you have to figure out the culture. Without a strong corporate culture centered around retention in insurance policy, maintaining employee loyalty will pose a challenge, making it considerably more arduous to establish an effective recruiting pipeline.”

General liability insurance for startups can play a pivotal role in addressing challenges stemming from both seasoned and fresh employees. Additionally, a surge in your workforce can swiftly reshape your company’s culture, though this rapid growth may not always be without its hurdles. Speed bumps, roadblocks, and delays are commonplace occurrences; therefore, it’s imperative to ensure you’re well-prepared.

When They Validate the Expense

Working with investors, you might have to purchase a D&O policy and errors & omissions (E&O) insurance, or otherwise known as professional liability. Venture capitalists won’t always work with you or have confidence in your company without these two. And for plenty of reasons, too.

First of all, they want to know you have the funds to cover your company if something goes wrong with the deal. Secondly, investors must protect their investment in your company. In other words, they want to include the members of their firm that serve on your board of directors.

To sum up, you might need to purchase various insurance coverage to secure funding. These purchases can make a uncomfortable dent in your general ledger. Unfortunately, the cost often pushes other essential insurance policies to the backburner, including EPLI.

When startups consider acquiring EPL insurance, the timing often hinges on a founder’s ability to justify the premium cost. Despite the inherent risks, some entrepreneurs choose to operate without EPL insurance, opting to navigate the landscape without establishing a robust safety net for employee issues. Rather than proactively addressing potential challenges, they rely on hope. This underscores the significance of incorporating insurance for startups, highlighting the need to secure comprehensive coverage and risk management strategies from the outset.

Naturally, this finger-crossing strategy isn’t favorable. Nor does it ensure your business’s longevity. Instead, acknowledging your exposure and validating the expense before a lawsuit occurs is the better option.

When They Have a Structured HR Dept

For startups and small businesses, a human resources (HR) department often consists of a few files in a drawer or your friend’s friend who needed a job. That said, HR departments aren’t usually the highlight of startups — but after reaching 20-25 employees, that all changes.

Employee issues begin to pop up as more team members are on board, inevitably changing your company’s culture. Plus, monitoring employee behavior becomes unpredictable, especially with multiple offices that don’t have any or enough on-site management. This scenario makes it tricky to know what’s honestly going on in the workplace and can increase the risk of an employment law suit.

It’s during this growth phase that many founders start shopping around for EPLI. It’s a founder’s one-two punch; get a structured HR department and then EPLI insurance — a knockout.

As mentioned earlier, company culture changes as the business grows. And your HR department plays a significant role in creating and maintaining positive company culture. This endeavor has become more relevant as a younger generation gravitates to the workforce. According to Forbes, 65% of 18-to-34-year-olds often consider culture before salary when searching for a new job.

Lastly, startups are ripe for plenty of lawsuits. Think about it; young, single individuals with irregular work hours tend to flock to startups. The typical “we’re all one big family, including your dog” startup environment is attractive, after all. And this group of individuals makes these companies flourish.

However, this unique blend can create a toxic concoction, too. Company time can blur into late nights and working happy hours, which often spells trouble in harassment claims.

What’s Next?

As your company develops, the establishment of a structured HR department — along with other milestones— should trigger the purchase of EPL insurance. If you’re exceptionally savvy, you’ll get this policy before running into any costly employee issues.

Understanding the details of what coverage your company needs can be a confusing process. Founder Shield specializes in knowing the risks your industry faces to make sure you have adequate protection. Feel free to reach out to us, and we’ll walk you through the process of finding the right policy for you.

In addition to EPLI coverage, young businesses should also consider specific insurance tailored to other unique needs. For instance, insurance for young drivers is crucial for startups that rely on young employees who drive as part of their job. Ensuring you have the right coverage can protect your business from unforeseen circumstances and provide peace of mind.

Want to know more about EPL insurance? Talk to us! You can contact us at info@foundershield.com or create an account here to get started on a quote.