Carl Niedbala

Managing Partner; COO & Co-Founder

Key Takeaways

Managing Partner; COO & Co-Founder

Healthcare providers lean on technology more today than ever before. Even before the current worldwide health crisis, virtual care and tele-health companies were developing rapidly. Since the start of the COVID-19 pandemic, patients have relied tremendously on their assistance due to lockdowns and social restrictions. However, fresh advancements also come with new risks. This post lays out industry exposures and how insurance can help support ongoing success.

Industry Overview

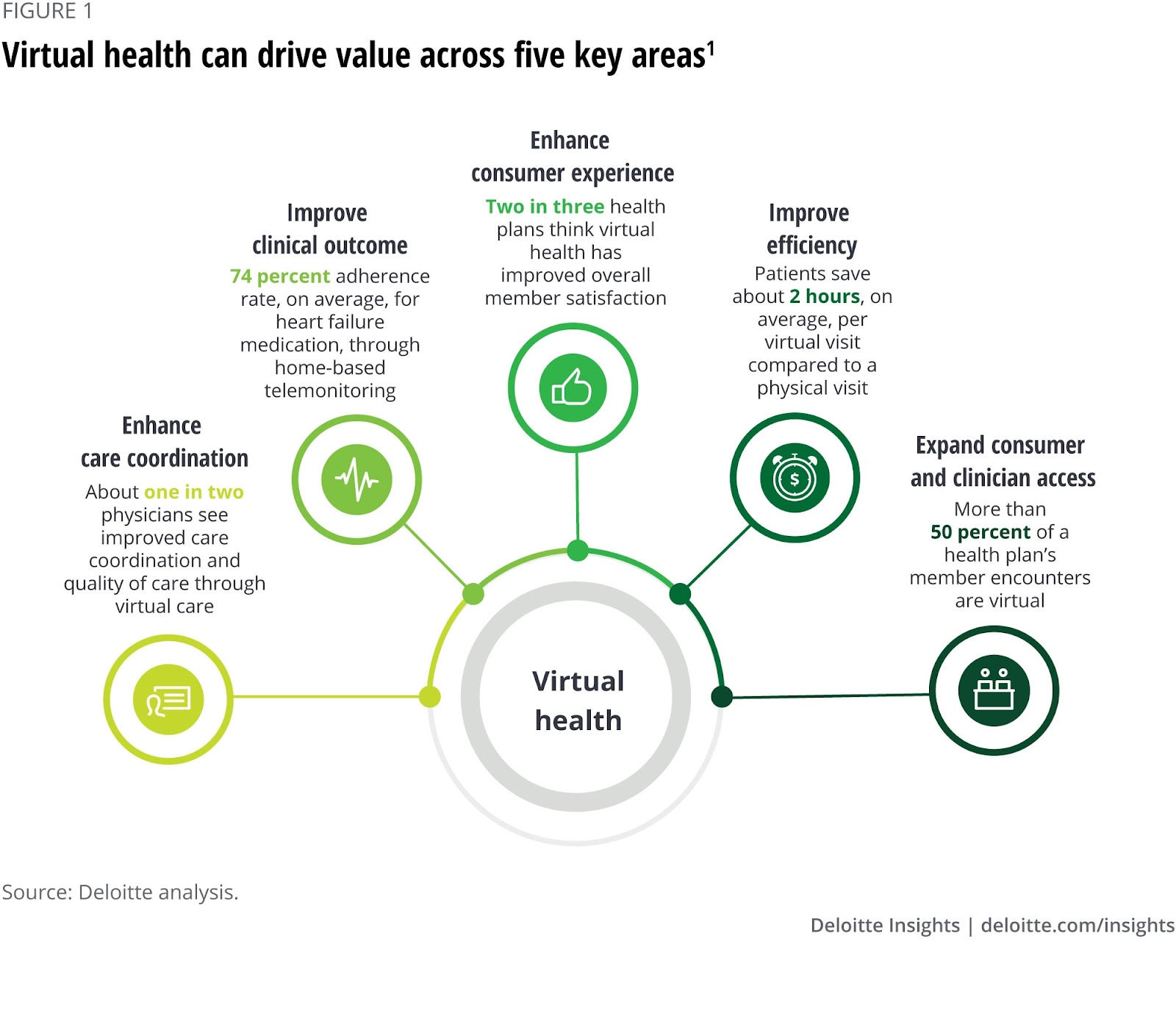

Technology in healthcare offers many benefits to providers and patients alike. For individuals who can’t access high-quality medical experts for any reason, technology offers these specialists at their fingertips. The virtual approach helps to expand access to healthcare for many people. So, it’s no surprise that this industry is growing in popularity and size.

For example, wearable medical devices and apps provide continuous monitoring for patients. Plus, this innovative tech offers healthcare providers real-time access to vital patient information. And people struggling with mental health conditions can receive treatment from a certified psychotherapist or counselor, no matter their situation.

That said, the US telemedicine market was valued at $45 billion in 2019 and projected to grow upwards of $175 billion by 2026. According to Forrester Research, more Americans are using telehealth nowadays, with healthcare telehealth visits likely exceeding one billion this year. Nearly 31% of healthcare organizations use video-based telemedicine currently, while 34% offer remote patient monitoring.

What’s more, Congress passed $8.3 billion in emergency funding earlier this year due to the COVID-19 pandemic. Some provisions eased the rules on using tele-health services, specifically on the US Medicare program. It’s safe to say that tele-health has undergone a phenomenal evolution recently. Some of the industries most significant players include:

- SnapMD

- Teladoc

- Zipnosis

- Doctor on Demand

- MeMD

- iCliniq

- Amwell

- MDlive

Biotech Risk Management Guide

What Risks Do Virtual Care & Tele-Health Companies Face?

Virtual care and tele-health operations aren’t new by any means. However, they’ve embraced such a massive evolution that identifying unknown risks is necessary to keep the pace of innovation. The following are a handful of exposures virtual care and tele-health companies face.

Cybersecurity

Conducting business operations online means navigating a slew of challenges, including dodging cybercriminals. These savvy outlaws are more sophisticated now than ever before, executing multi-tiered attacks on any company with the slightest vulnerability.

Unfortunately, virtual care and tele-health companies encompass plenty of risks merely because of the nature of their work — and healthcare is the most expensive industry. For example, a cybercriminal could easily hack a patient’s medical device, allowing entrance into the entire company’s network.

With the price tag of a cyber attack over $1 million and a data breach averaging nearly $4 million worldwide, any company would do itself well to maintain adequate cybersecurity.

Product failure

We’ve seen an uptick in remote patient monitoring and wearable technology in the past few years. These services will likely continue playing a prominent role in healthcare. Yet, what happens when they fail?

Suppose there is a service disruption to a medical technology company, impeding the app monitoring a patient’s blood sugar levels. When the app fails to notify the patient of dropping blood sugar levels, they might face a severe medical emergency (i.e., hypoglycemic shock or coma).

Naturally, when the product fails for a virtual care or tele-health company, it often causes significant implications, such as financial or reputational loss. This damage is aside from health declines experienced by the patient, which frequently call for monetary compensation.

Technology failure

In thinking of virtual healthcare, technology is the first thing to come to mind for most people. Like tech products, though, what if technology fails us all together? These companies rely so heavily on technology to carry out flawless orders that any failure can shake things up in an awful way.

Perhaps a kiosk in a pharmacy or local shopping center misreads a patient’s weight. Because of this malfunction, a healthcare practitioner prescribes the wrong medicine dosage. Plenty of outcomes could happen, such as worsening symptoms or even an overdose. Unfortunately, the mistake all stems back to the accuracy of the kiosk’s technology — which failed.

Misunderstanding or miscommunication

Another overall risk for virtual care and tele-health companies is that the patient and provider don’t communicate properly. Perhaps the connection was fuzzy, or there was a language barrier. No matter the reason, this particular risk is massive.

For example, what if a psychotherapist provides online treatment for a patient with chronic depression. The therapist misunderstood the severity of the patient’s state and didn’t realize the treatment wasn’t sufficient for that specific moment. The worst-case scenario is that the patient attempts suicide shortly after the therapy session.

A common real-life scenario for a digital health company involves an after-hours nurse misinterpreting a patient’s condition, leading to an unexpected visit to the ER on the patient’s end. While communication through phone or video chat offers convenience, it’s not infallible, presenting the daily challenges that virtual care and telehealth companies grapple with.

What Insurance Do Virtual Care & Tele-Health Companies Need?

Any company that delivers healthcare services electronically benefits from the safety net of insurance coverage. With such rapid developments for these businesses, it’s vital to secure the best coverage for the unique risks they face. The following are some crucial policies no virtual care or tele-health company should go without.

General liability (GL) insurance

Doing business in any industry results in facing several fundamental risks, such as the notorious “slip-and-fall” claims. However, when it comes to damaging a third party’s property or facing a products liability claim, a general liability policy is what you want in your corner. Most virtual care and tele-health companies consider GL insurance to be the foundation of protection for building a robust risk management plan.

Errors and omissions (E&O)

Also known as professional liability insurance, E&O steps in to protect you from lawsuits claiming that your product or service didn’t perform as expected according to the customer and industry standards.

Cyber and media liability

This policy works to protect virtual care and tele-health companies against third-party lawsuits that arise from digital activity. Cyber insurance also helps to cover fines and penalties from regulators.

Property insurance

Property insurance protects your tangible property as well as the contents of the building itself. Consider the cost of replacing office supplies, high-end computer equipment, and cables after a weekend office fire or catastrophic storm.

Understanding what coverages your virtual care & tele-health company needs can be a confusing process. Founder Shield specializes in knowing the risks your business faces to make sure you have adequate protection. Feel free to reach out to us, and we’ll walk you through the process of finding the right policy for you.

Insurance Rebuilt, End-to-End