Jonathan Selby

General Manager; Technology Practice Lead

Key Takeaways

General Manager; Technology Practice Lead

Social media influencers face unique and evolving risks, more than a pure “media” exposure, their content, “likes,” and endorsements run across a hundred different industries (or more!). Encouraging consumers to buy a particular product or service means featuring their online “opinion” front and center. As a result, these individuals must learn to navigate liability exposures with finesse, especially since these exposures can come from different sources. Here’s why social media influencers need the protection of influencer insurance.

What Is a Social Media Influencer?

Social media influencing and the personalities called “influencers” have grown exponentially over the last 5+ years. Scroll through any feed on any of your devices, including your TV, and you are bombarded with products and services promotions.

Once relatively limited to high-profile individuals, such as celebrities or trusted experts, influencers now include anyone with enough followers and an exciting post to attract attention. Of course, not all stars are influencers, and not all influencers are celebrities — they aren’t the same. Regardless of their official status, though, online influencers are responsible for swaying consumers’ buying decisions.

It’s not uncommon for influencers only to impact one particular niche or group of people, such as a subculture or specific age group. They tend to post lots of photos while wearing or using the featured product or service. Additionally, influencers typically gain their online followers by featuring content relating to a subgroup or niche instead of merely “being popular” like a celebrity. And what attracts the most attention? Something edgy? Cutting edge? Merely clever?

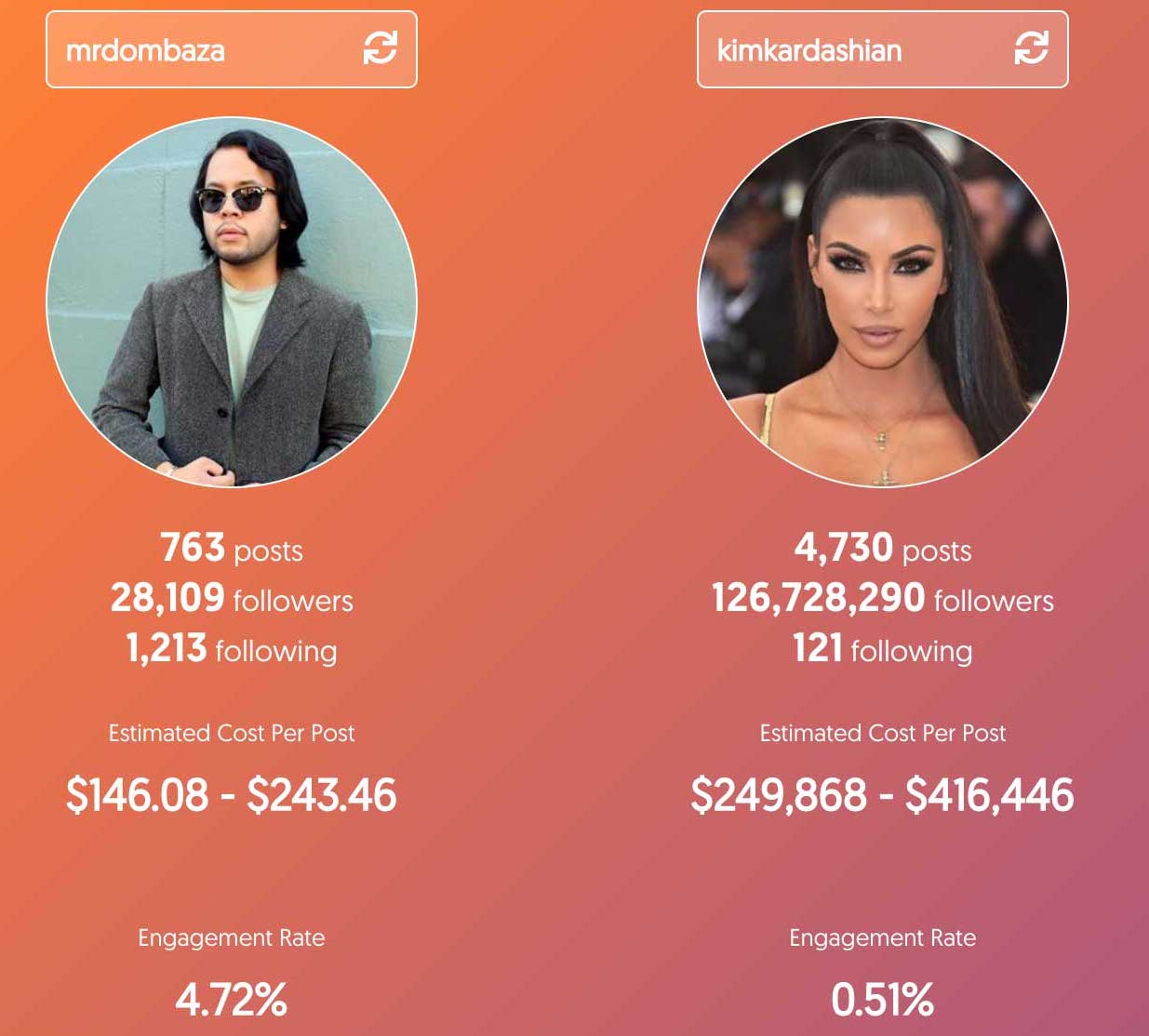

For example, the graphic below illustrates how globally-known celebrities don’t always have the most significant influence. Although Kim Kardashian is known worldwide, the San Francisco musician Dom Baza has more power in his specific domain.

That said, content creators dominate many social media channels, including Twitter, Instagram, Facebook, etc. Plus, influencer marketing becomes more popular with each passing day. Plenty of brands lean heavily on this strategy as it’s affordable and successful. A current trend is for brands to avoid massive influencers but partner with “nano-influencers” or micro-influencers instead.

You may not know them all, but some of the most significant influencers across multiple channels are:

- Zach King

- PewDiePie (aka Felix Kjellberg)

- Cameron Dallas

- Cristiano Ronaldo

- Kayla Itsines

- Selena Gomez

- Kylie Jenner

- Huda Kattan

What Risks Do Social Media Influencers Face?

One word could potentially sum up the risks of social media influencers: lawsuits. However, it’s not that simple. We live in a litigious society, and many people sue at the drop of a hat. Not only does our American culture accept this approach, but we also tend to embrace it.

When influencers create social media posts for hundreds of thousands of people to see, there’s a good chance that someone will find something they consider actionable. If it isn’t catchy and even controversial, a campaign may not attract the number of views a brand targets.

As an influencer, people might view your influence as inauthentic or misleading. Perhaps the product didn’t work for them as well as it did for you. Maybe someone other than the brand that engaged the influencer owned the product or method.

Defamation

On the flip side, maybe someone claims that you ripped off their brand or defamed their reputation. Whether purposefully or unintentionally, defamation claims are a notable concern for influencers. What’s more, influencers must prioritize staying on the right side of the law. In other words, transparency is a must — but it’s not always followed to a T. Slander and libel are two widespread issues social media influencers must watch closely, as well.

Personal Injury

Social media influencers are not immune to influencer lawsuits. While they may not have to worry about physically injuring themselves on the job, they can still face legal trouble for their actions online. One type of lawsuit that influencers can face is an influencer lawsuit, which is a legal claim alleging that an influencer has caused harm to a business or person through their advertising or endorsements.

Regulations

For example, the Federal Trade Commission (FTC) recommends influencers to use the #sponsored or #ad hashtags to identify sponsored content. However, only about half of influencers put those hashtags to good use. A handful of influencers never label their content whatsoever. And that’s just for starters — the FTC has plenty more poorly-followed regulations begging for legal ramifications.

Content Creator Insurance Guide

Authenticity

Aside from the legalities of influencer marketing, influencers must maintain an aura of authenticity for brands to continue to work with them. Otherwise, influential posts are merely lost among the endless online chatter. Copyright issues are a massive concern, too.

Navigating morality conflicts poses a risk that influencers must accept. What if, as an influencer and individual, you make a mistake? Suppose your actions or behavior diverge from the brand’s values. This could lead to the company dropping you as their influencer, introducing revenue challenges and potential legal issues, highlighting the importance of embracing and managing the risk accept aspect in such situations.

Real-Life Lawsuits

- Superintendent George Coffman sought $225,000 in damages after suing Oklahoma mom, Susan McNair, for defamation. Additionally, the case included an accusation of “intentional interference with contractual and business relationships.”

Read the full story here: 3 Publicized Legal Cases Involving Social Media Use

- A sarcastic two-word social media response (“Actually, yeah”) resulted in a seven-week school suspension and potential felony charges for 17-year-old Reid Sagehorn. Three years later and loads of litigation, Reid won a $425,000 settlement for the tweet charges.

Read the full story here: Rogers student wins $425K in tweet

- After striking a deal with Grown-ish star Luke Sabbat, Snapchat regretted the contract — mostly because Sabbat didn’t hold up to his end of the deal. So, Snap Inc. is seeking a $45,000 settlement for damages to recoup the initial contractual payment and another $45,000 for damages.

Read the full story here: Snapchat’s PR firm sues influencer for not promoting Spectacles on Instagram

5 Reasons Social Media Influencers Need Insurance

1. Others Require It

It’s not uncommon for businesses to require their contractors to carry various insurance policies. Companies who hire social media influencers are no different. What’s more, most professionals have learned quickly that social media exposure is risky. Therefore, influencer marketing is equally as risky.

Influencer insurance transfers this particular risk from the company that hired the influencer back to the influencer. With this added safety net, managers are more likely to sign a contract with a social media influencer.

2. Brands Want It

Besides companies requiring social media insurance before joining forces with an influencer, most brands genuinely want it. Having an insurance policy in your corner speaks volumes.

Although your influencing abilities might have been legit without insurance, adequate coverage legitimizes your professional endeavor in the eyes of company leadership. Brands that engage influencers or agencies to provide influencers won’t even get a shot to bid on a project without insurance. On direct, brand-to-influencer campaigns, you will start seeing insurance as a contract spec.

3. Defamation Accusations

Libel and slander are two of the most widespread defamation accusations. Libel is when someone accuses you of writing a false or harmful statement about them. Slander is when you say those same things out loud, such as in a video.

Naturally, it’s never a bad idea to follow your mom’s advice to “play nice,” although playing nice means different things to people. If you face one of these lawsuits, influencer insurance helps cover legal defense costs and settlement fees.

You may have heard that “opinions” are safe from lawsuits — “it’s only my opinion” — however, that doesn’t mean you won’t get sued or threatened with a suit if your “opinion” is taken the wrong way. Influencer liability insurance provides you with a lawyer to defend even baseless claims.

4. Online Disputes

It’s no news flash that sometimes people will disagree with your thoughts and opinions. It doesn’t matter if what you present is backed by hundreds of years of scientific research; some soul can find an issue with it.

As a result, the internet makes these offenses effortless to commit. The “backbone” of Influencer insurance is “media liability” — we’ve just customized it further for the influencer media spec. The insurance works to address the expenses resulting from these common lawsuits.

5. Worldwide Liabilities

The fantastic thing about social media is its worldwide reach. Conversely, the downfall of social media is its worldwide reach. In short, influencers don’t typically impact only a small local crowd. As an influencer, your words could travel around the world multiple times. This global approach means potentially crossing more cultural boundaries than many individuals expect.

Social media influencers run the gamut of risk from personal injuries to defamation to online disputes every day. It’s vital to have adequate insurance coverage to keep your influencer endeavors in business for the long haul.

One great example to keep in mind is something called a “takedown” request or demand. Suppose you wear a t-shirt with a graphic image in an online video. Do you know who owns the rights to use the image on the t-shirt? If you receive a demand to take down the photo you’ve posted to social media, do you know how to do that and ensure compliance with international laws?

Understanding the details of what coverage you or your company needs can be a confusing process. Founder Shield specializes in knowing the risks your industry faces to make sure you have adequate protection. Feel free to reach out to us, and we’ll walk you through the process of finding the right policy for you.

Insurance Rebuilt, End-to-End