Kyle Jeziorski

Senior Director, New Business & Placement

Key Takeaways

Senior Director, New Business & Placement

If you’ve caught a glimpse of any news, you already know that claims arising against directors and officers are more widespread now than ever before. Over the past five years, a whopping $23B was the cost of securities litigation—which is the most prevalent lawsuit nowadays. What this has created is an increase in risk exposure for directors and officers (D&O) insurance.

In a previous post, we looked in-depth at exclusions in D&O policies (here’s the post). Here, we’re driving on the other side of the road by examining some D&O insurance endorsements that will benefit your company.

What’s an Insurance Endorsement?

Naturally, before we start listing what endorsements you need, let’s clarify what we mean by “insurance endorsement.” Also known as a rider, add-on, or enhancements, endorsements modify a commercial policy by adding, deleting, or excluding specific types of coverage.

Instead of having to purchase another separate policy, endorsements let you tailor your current D&O policy to fit your particular needs better. Not only does it save you from having to shop around for more plans, but it also saves on the cost of insurance as a whole.

Endorsements are vital because not every company follows the same business model. Therefore, the exposure your company faces is unique to you. A “missing piece” in a D&O policy might leave your business wide open for costly lawsuits. Endorsements work to create more comprehensive coverage, customized to your professional needs and budget.

Why Do You Need Them?

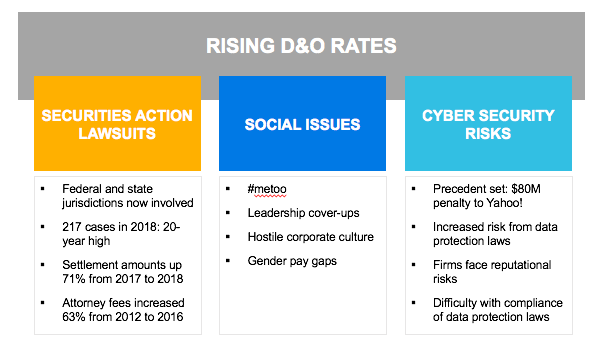

D&O insurance can cover many claims against a company for the action of its directors and officers. With such litigation on the rise, however, a few D&O insurance trends have surfaced in the space, including Securities action lawsuits, Social issues, Cybersecurity risks, and EPL D&O claims. To protect your company from costly defense and settlement costs, purchasing adequate D&O insurance is essential.

To protect your company from costly defense and settlement costs, purchasing adequate D&O insurance is essential. As you might have imagined, a D&O claim isn’t cheap. On average, you can count on paying lawyers $35,000 to $100,000 to defend each incident—but that’s just the minimum. And if the legal fees aren’t jolting enough, indemnity payments average about $500,000, but can easily reach seven figures.

That said, D&O coverage only works in your favor if you have the right exclusions and endorsements in the policy. While exclusions carve away at extensive coverage, endorsements work to fill in the gaps and customize the overall plan. These add-ons can beef up your D&O policy so that you minimize your vulnerabilities to a manageable level.

What are Common Endorsements in a D&O Insurance Policy?

Additional Side A limit

If an insured exhausts the rest of the policy, some insurers offer additional coverage for Side A claims only. Of course, this endorsement only comes into play when there are still outstanding claims against individuals.

Dilution claims

Sometimes, shareholders believe that a significant round of funding unfairly diluted their stake in the company. The problem is that most D&O policies don’t cover this issue of “watering down”—but that doesn’t stop unhappy shareholders from suing. With this particular coverage enhancement, the insurer can offer a sublimit to use for defense costs related to these claims. Keep in mind that this endorsement typically only applies to claims from former executives.

Bump-up claims

It’s not uncommon for shareholders to feel dissatisfied with an acquisition deal. Often, the shareholders and board of directors don’t agree on the sale price of the company. In these unfortunate situations, shareholders frequently sue for the difference. These suits are known as “bump-up” claims and are often excluded in D&O coverage. However, they are rather complicated and tend to show up in endorsements—sublimited and usually on a defense cost-only basis.

Employed lawyers

In the realm of public company D&O insurance, in-house counsel may frequently find themselves embroiled in a D&O lawsuit due to their association with your company. Nevertheless, conventional D&O policies may not consistently extend coverage to them for their contributions to your insured company. The solution? By specifically including “in-house counsel” within the insured definition, this add-on precisely addresses this issue.

Class certification investigation

For a lawsuit to become a class-action lawsuit, a judge must certify plaintiffs as a “class.” But before that, the plaintiff must argue their case and undergo an investigation. Once the claim is deemed a class-action lawsuit, the cost of litigation skyrockets. Some insurers will include a sublimit to help pay for these specific class certification investigation costs.

Roadshow coverage

Before an initial public offering (IPO), founders form relationships with investors by using various presentations and pitch decks. Roadshow coverage chisels away at the IPO exclusion, allowing coverage for claims arising from alleged misinterpretation during the time frame leading up to an IPO. However, coverage doesn’t depend on whether or not the company ends up going public.

Broad change in control and M&A provisions

Companies undergo a change in control and transitions continually. But when too much change occurs, some insurers will drop their coverage. For example, if a third party acquires a significant percentage of voting shares or assets, the policy might go into run-off or end coverage entirely. Or, if the company makes an acquisition, but in doing so, it exceeds particular thresholds, such as revenue, assets, employee count, etc. In this case, coverage may change—which is why higher limits benefit companies so much.

Duty to notify triggered upon written notice to CFO, CEO, or General Counsel

Only a few people per company should be allowed to report something to the insurer. Namely, the CFO, CEO, or General Counsel. Otherwise, things get messy; the more “gatekeepers” there are that hold such knowledge and responsibility.

Pre-arranged ERP (“Tail”) Pricing

An extended reporting period (ERP) is an endorsement you can add that allows you to report claims ever after your policy expires. It’s frequently known as “tail” coverage, as well. A basic ERP is typically 30-60 days, but it’s possible to extend it for several years or even renew it with an additional fee.

Liberalization Clause

This policy provision — a liberalization clause — offers a policyholder enhanced benefits when existing coverage changes to comply with new laws and regulations. Typically, coverage doesn’t experience a massive overhaul; it’s merely a new edition of identical insurance and comes without any additional cost.

Extradition Coverage

When someone requests the conviction of an insured person, this add-on provides the funds needed to oppose, challenge, and resist or defend (including appeals) the request for extradition.

What Do D&O Insurance Endorsements Cost?

When you consider endorsements the building blocks of your D&O insurance policy, it’s more natural to accept any additional costs they might accrue. Although endorsements come in all shapes and sizes, their affordability might surprise you.

Remember, including an endorsement isn’t the same as buying a whole new policy. Endorsements create a fresh, customized policy—but without the new car sticker price, per se. Working with a knowledgeable insurance expert can help land you the best policy for your company.

Understanding the details of what coverage your company needs can be a confusing process. Founder Shield specializes in knowing the risks your industry faces to make sure you have adequate protection. Feel free to reach out to us, and we’ll walk you through the process of finding the right policy for you.

Want to know more about D&O insurance? Talk to us! You can contact us at info@foundershield.com or create an account here to get started on a quote.