Jonathan Mitchell

Financial Industry Lead

Key Takeaways

Financial Industry Lead

With the world practically turned upside down by COVID-19, remote work has, to varying degrees, become the “new norm.” Many individuals have been working from home for years already, such as virtual assistants, travel agents, freelance writers, etc. However, a new wave of remote working arrangements due to the pandemic has caused employers to rethink their traditional operations. In this post, we take an honest look at employment practices liability (EPL) insurance and how this landscape is changing to fit a remote world.

What Is EPL Insurance?

EPL insurance, otherwise known as EPLI, is coverage protecting companies against employee lawsuits surfacing from their employment conduct practices. If an employee files a lawsuit against you — even if the allegation is baseless — EPL insurance covers your defense costs. Additionally, companies frequently couple EPL insurance with directors and officers (D&O) insurance for secure, 360-degree protection.

Some of the most common accusations in EPLI are:

- Discrimination

- Sexual (or another workplace) harassment

- Wrongful termination

- Failure to employ or promote

- Breach of terms of an employment contract

- Negligent evaluation

- Wrongful discipline, bullying

- Wrongful infliction of emotional distress

It comes as no surprise that having employees creates more vulnerabilities for company leaders to manage. What’s more, government regulations provide employees with access to administrative claims and litigation. A successful plaintiff using the laws to back up their claims can have their legal costs paid by the employer even if they only win $1. Our litigious society usually accepts this approach without reserve.

Consider the recently trending employment claims, including gender discrimination, unequal pay, the #MeToo movement, and religious and other “freedom of expression” claims — heck, even the employers’ need to accommodate employees with disabilities like stress (and the use of medical marijuana) qualify. Add the strain on workers and employers caused by the coronavirus pandemic, and the workplace (remote or not) becomes even more complicated to navigate.

Understanding the Pandemic’s Impact

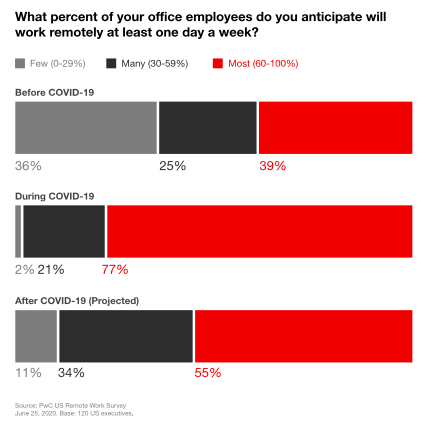

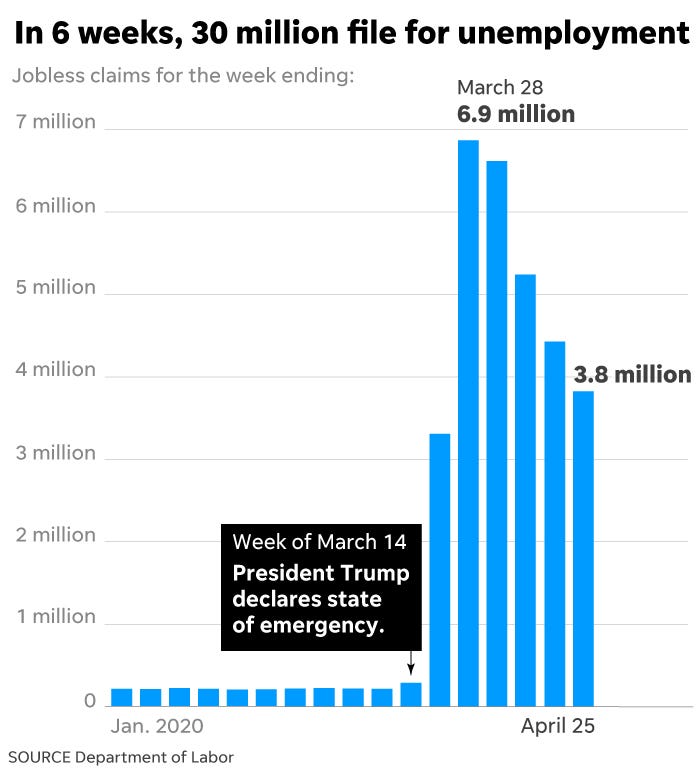

When COVID-19 hit our shores early in 2020, it shook the global economy. The pandemic touched every industry, forcing many companies to shutter, reduce their workforce, or send employees home to work. Naturally, not all industries had the option of remote work — but those that did, tried to tackle it head-on.

Some financial experts questioned whether the downturn was solely because of COVID-19 or if it was merely a long time coming. No matter who or what is to blame, the fact is that everything changed seemingly overnight, including how people handle issues with their employer.

Keep in mind that most companies tend to purchase or beef up their EPL insurance before a significant transformation. We feature a helpful article on the matter here: When Do Startups Typically Purchase EPLI Coverage? But this pandemic didn’t offer us the luxury of a heads up, per se. These unfortunate dynamics left most companies grappling with a harsh financial reality — and more work-at-home employees.

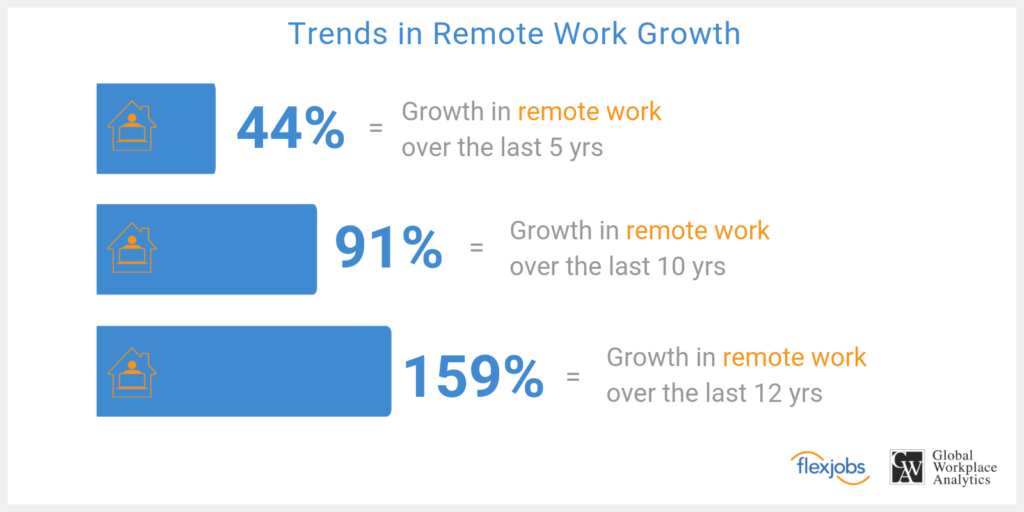

Interestingly, over half of Americans want to keep working from home after the pandemic. Furthermore, two-thirds of businesses intend to maintain a version of their remote policies permanently. Google, American Express, Airbnb are among the many major companies to extend their policies. Plenty more companies are following their examples or are offering their employees greater flexibility in their schedule.

A successful, remote-friendly approach to work has many positives, such as:

- Better work/life boundaries

- Increased productivity

- Less commute stress

- Positive environmental impact

- Improved employee retention

- Increased job satisfaction

- Better use of technology

However, when it comes to policy retention in insurance, working from home isn’t always a walk in the park. Managing tasks like collaborating with fellow team members and balancing childcare or eLearning can pose considerable challenges for most employees in the realm of remote work. And this is just scratching the surface. With the pandemic-induced transition from on-site work to remote setups, many companies are bracing themselves for a potential influx of employment claims.

Potential EPLI Issues Surfacing

Unquestionably, remote work offers plenty of benefits to individuals, families, and communities. Employers and businesses can thrive more with a happy and satisfied workforce — but remote work isn’t for everyone.

Some employees have significant issues working from home, and these barriers can put them and their employers in a bind. Plus, some companies haven’t recovered fully from the pandemic’s impact, causing them to tighten their limitations. Both sides, employers and employees, have valid complaints and concerns about current dynamics. Here are a few of the most common issues experts predict will take precedence in the coming days.

Wage Issues

In conjunction with COVID-19, a new overtime rule was changed and put into effect at the beginning of the year. It had been untouched for 15 years, so the transition has been complicated. Add in remote work, and employers are scrambling to keep up with the unprecedented shift.

“The Department of Labor estimates that 1.2 million additional workers will be entitled to overtime pay as a result of the increase to the standard salary level, while an additional 101,800 workers will be entitled to overtime pay as a result of the increase under the highly-compensated employee rule.”

Insurance Journal

Employers are faced with several wage issues now, including accurate time-tracking, correct overtime compensation, proper employee categorization, and compliance with the Fair Labor Standards Act (FLSA). As more and more employees educate themselves on old and new laws, we expect to see an uptick in employment practices lawsuits. Plus, remote work often means employees feel “on the job” for more hours than usual — and they want compensating for it.

Some employers have announced pay freezes in reaction to the pandemic, and still, others have required pay cuts — a drastic measure designed to keep a struggling company from shutting its doors altogether. These scrooges argue that reduced wages don’t impact the bottom line if an employee saves commutation and related expenses. Bah humbug. Can you see the claims coming?

Wrongful Termination

Most employers have tried to navigate the pandemic as best as possible. Hard-hit industries faced tough decisions and reduced their workforce significantly — which will likely spark a wave of wrongful termination claims. Companies can try to conduct a reduction in force (or “RIF”), but these have a bushel full of compliance requirements. Even companies that try to undergo a “neutral” (as to tenure, age, gender, etc.) RIF can get caught in the middle of an employment claim for wrongful termination.

For example, some employees were terminated after raising concerns about safety in the workplace. Others lost their jobs after obeying the shelter-in-place orders, refusing to go back to work, or working from home longer than an employer wanted. And still, others stayed home from work, battling the novel virus.

As you might imagine, wrongful termination during COVID-19 is a muddied area to address. Timelines and causes present multiple challenges. Nevertheless, This era will likely launch an onslaught of employment practices lawsuits.

ADA Discrimination

As employers nationwide try to steer through the pandemic, they encounter challenges protecting their workforce’s safety and health. After all, safeguarding your employees isn’t always clearcut. Complying with federal laws, such as the Americans with Disabilities Act (ADA), makes any attempt to navigate that much more complicated.

The US Equal Employment Opportunity Commission (EEOC) has published, What You Should Know About COVID-19 and the ADA, the Rehabilitation Act, and Other EEO Laws to help guide employers through this complicated timeframe. But employment practice claims are still going to surface based on ADA discrimination charges. What an employer can and can’t do often seems like a shady area, mostly because of ever-changing rules — especially when it involves COVID-19.

EPLI Changes to Expect After COVID-19

When the virus hit, many people expected insurance carriers to update their policies swiftly by adding a pandemic-like exclusion on every policy known to humankind. Of course, enforcing an update of this caliber would have induced an “end of times” scramble. Most insurance carriers didn’t join the supposed exclusion wave, although some carriers rewrote their policies to include pandemics. It’s safe to say that this approach was not a widespread movement.

Slow Renewals

However, companies should expect the renewal process to move more slowly than usual. Applications will likely include virus-related questions as underwriters proceed cautiously. Public companies should prepare for more transparency, as well, focusing on public disclosures. Private companies should plan to have their financial stability thoroughly examined (i.e., debt management, funding preparation, etc.)

Increased Claims

This article delves into the repercussions of the growing prevalence of remote work on employment. Simultaneously, EPLI insurers are grappling with mounting EPLI claims, triggered by factors such as the general economic downturn, challenges in fostering diversity and inclusion, the influence of the Black Lives Matter movement, and the #MeToo movement.

Furthermore, there is so much uncertainty in the economy, that even usually trustworthy predictors, like the US Bureau of Labor Statistics (BLS) which offers its ten-year, three-year, and industry by industry forecasts has yet to amend its 2019-2029 statistics and surveys, despite the enormous impact COVID-19 has had on the economy.

Coverage Transition

Insurers who have written large books of EPLI for years are pulling back their capacity to issue EPLI policies due to prior losses and increased exposure in industries, such as hospitality (i.e., restaurants, hotels, sporting arenas, etc.). Those insurers who still have the stomach for EPLI will push rates up, add coverage limitations, and increase claim deductibles, to name a few ways the coverage will likely change.

EPL insurance coverage is essential, and usually comes with value-added services to make your company a “better risk,” including:

- Free “ask an expert” hotlines

- Resources such as “build your handbook”

- Access to policies and procedures

- Anti-harassment and similar training

These value-adds usually cost nothing and, in the eyes of insurers, make your company less claims-prone.

Navigating the intricacies of determining the coverage your company requires can indeed be a daunting process. At Founder Shield, we specialize in comprehending the specific risks inherent to your industry, ensuring you have the adequate protection you need. Don’t hesitate to reach out to us, and we’ll guide you through the process of finding the right policy tailored to your unique needs. With our expertise, we can help you understand how can risk be reduced effectively, providing you with peace of mind and confidence in your insurance coverage.

Lastly, check back in with us here as we will be updating the resources we provide and are generally available to employers.

Want to know more about EPL insurance? Talk to us! You can contact us at info@foundershield.com or create an account here to get started on a quote.