Jonathan Mitchell

Financial Industry Lead

Key Takeaways

Financial Industry Lead

As a manufacturer, trader, or service provider, how do you protect your balance sheet from losses due to non-payment? If you’re like many professionals, you might lean on a credit agency to chase down customers in arrears—but that has a price tag of its own. Often customers do not pay invoices timely or are unable to pay because of a bankruptcy, which only harms your balance sheet. In this post, we cover how a trade credit insurance policy can safeguard your balance sheet and assets by paying out a percentage of the outstanding debt.

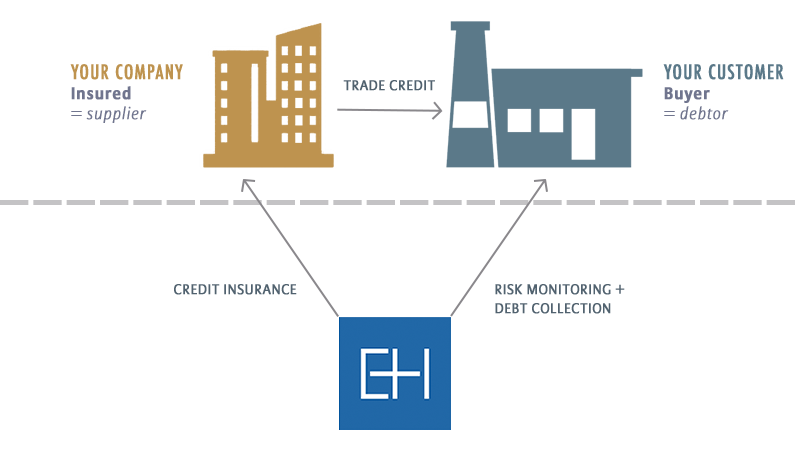

What Is Trade Credit Insurance?

Trade credit insurance is a type of coverage that targets the delinquent accounts receivables area on your company balance sheet, helping to recoup those particular losses. Whether it’s because of insolvency, bankruptcy, or human error, mounds of debt go unpaid every day. When your business is expecting a payment or payments that never arrive, it only sets your financial outlook back a few paces. Trade credit insurance works to make this setback less harmful.

Let’s look at the numbers; one in ten invoices become delinquent. What’s more, is that accounts receivables usually make up over 40% of a business’s assets, making negligent customers a source of severe financial stress. Trade credit insurance works to alleviate this stress by covering some of the debt that customers won’t (or can’t).

This coverage can help to prevent bankruptcies and manage credit. In doing so, trade credit insurance offers companies more opportunities to expand, connecting locally, nationally, and globally.

The International Credit Insurance & Surety Association clarifies, “If a buyer does not pay, the trade credit insurance policy will pay out a percentage of the outstanding debt. This percentage usually ranges from 75% to 95% of the invoice amount, but may be higher or lower depending on the type of cover that was purchased.”

How Is Coverage Typically Structured?

Like many types of coverage, trade credit policies are typically flexible. The policyholder can choose to cover the entire portfolio or a handful of significant accounts. What this means is that companies can customize ways to protect against losses stemming from corporate insolvency, bankruptcy, and financial liabilities.

Here are some of the most popular policy structures for trade credit insurance:

- Multi-Buyer – Covers all customers; the more substantial portion of risk share between the carrier and insured.

- Named Customer- Covers specifically requested customers; usually used when there are several customers with broad exposure, risk share terms are more flexible.

- Single Customer- Covers only one customer, usually used by companies that have one individual customer that accounts for a significant portion of revenue that, if left unpaid, could expose the company to bankruptcy. Very flexible.

Who Needs Trade Credit Insurance?

Trade credit insurance offers multiple benefits to companies across numerous industries. Unfortunately, most companies choose to forgo this coverage and opt to self-insure. While self-insuring isn’t fundamentally flawed, this strategy does tie up capital that could be used for other things, such as developing the business or launching new products.

Furthermore, many self-insuring companies find themselves in a bind when experiencing a credit crunch. But by then, it’s too late to add coverage. A better approach is to obtain trade credit insurance before you’re in hot water. Not only will this improve your long term risk management strategy, but it will also allow your company room to expand comfortably.

Benefits

However, this coverage is more than merely a financial safety net. If you’re not sure how this coverage could profit your business, consider these benefits:

- Rapid expansion – Many companies shy away from upselling to current customers or trying to obtain new customers because it’s too risky. When accounts receivables are insured, however, companies are freer to expand their sales.

- International development – Taking your business global opens exciting new markets, but also introduces unique risks. Trade credit insurance can be a valuable tool in your risk management toolbox, helping you navigate the challenges of international development and achieve your export goals.

- Sales increase – Even if a policyholder never files a claim, a trade credit insurance policy can counterbalance its own cost over and over by supporting risk-free sales expansion.

- Better rapport – When it comes to lending more capital, and at a better rate, banks tend to favor companies that have insured accounts receivable—some even require it for various loan qualifications.

- More capital – This policy lets you free up money that would have otherwise been used to beef up your bad-debt reserves.

- Tax-deductible – Trade credit insurance premiums are tax-deductible. Bad-debt reserves are not.

- Increased protection – Non-payment and catastrophic loss is always a fear in the world of business. Often, these circumstances are unexpected. However, this coverage helps to make these situations far less crushing.

Understanding the details of what coverage your company needs can be a confusing process. Founder Shield specializes in knowing the risks your industry faces to make sure you have adequate protection. Feel free to reach out to us, and we’ll walk you through the process of finding the right policy for you.

Want to know more about trade credit insurance? Talk to us! You can contact us at info@foundershield.com or create an account here to get started on a quote.