Carl Niedbala

Managing Partner; COO & Co-Founder

Key Takeaways

Managing Partner; COO & Co-Founder

Update: We’ve released a new whitepaper examining the Biotech industry. We dive into the insurance landscape, funding, legal climate, and how to approach risk management for companies in this sector. You can download the report here!

Most life sciences professionals understand the FDA drug-approval process. Or, at least, you are aware of how painstaking it is to undergo such a venture. But things can get a little muddied amid all the regulations and requirements. In this post, we focus on what happens during Phase 3 and how you can protect your company while navigating this specific part of the process successfully.

FDA Trials Process Overview

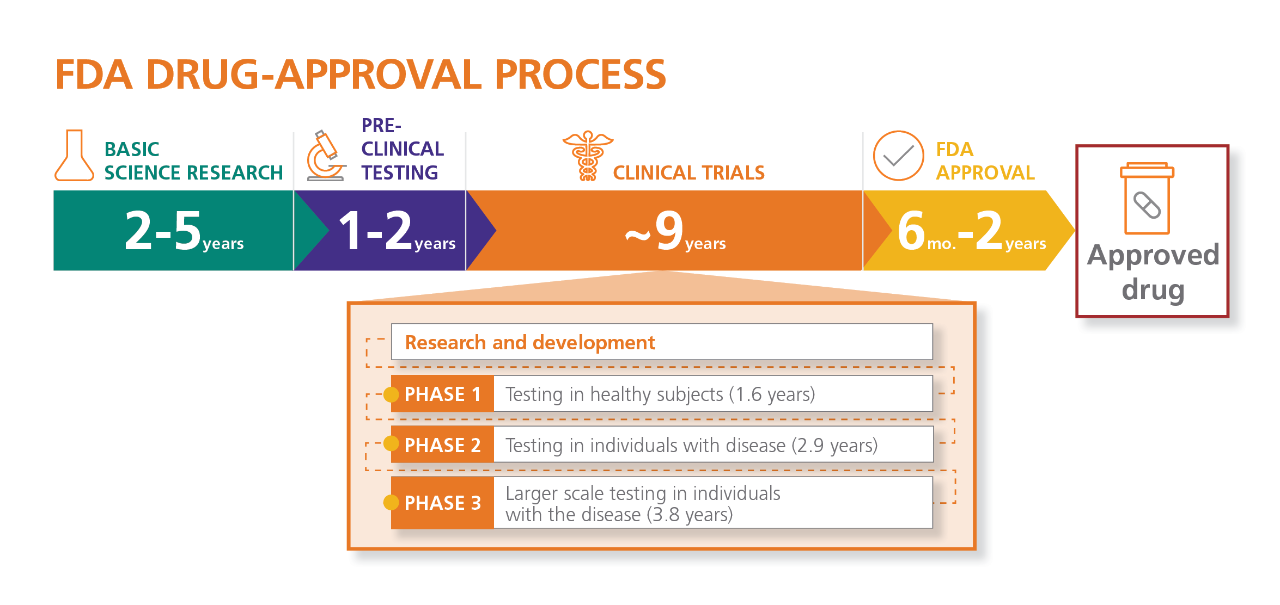

The path from the research and development (R&D) phase to releasing a new FDA-approved drug on the market is drawn-out — averaging 9-15 years. As a result, some refer to the FDA-approval process as “the most stringent in the world.” Despite its slow-moving procedures, the FDA strives only to approve safe and effective medicine.

Aside from the prolonged pace, it’s costly, too. The average price tag to develop a new drug is over $2.5B. Because the costs remain high, some are pushing to speed up clinical trials to release drugs faster and to help cut costs. However, substantial debate among biotech executives over this fast-tracking approach is causing somewhat of a rift in the industry.

Nevertheless, the FDA trials process consists of the following phases:

- Phase 1 – This phase involves using healthy individuals to ascertain a drug’s fundamental properties and safety outline in humans.

- Phase 2 – Clinical trials administer the drug to volunteers of the target population. The FDA uses results from this phase to determine the protocol for the next phase of trials.

- Phase 3 – The third part of trials is the most substantial and most expensive phase, involving a significant amount of real-life patients with the disease. Treatment IND and parallel tracking sometimes accommodate this phase.

- Phase 4 – The shortest and most anticipated step is the fourth one, often taking a mere six months to reach approval status. Directly before a stamp of approval, the FDA uses this phase to conduct a final review of the findings.

- Phase 5 – This phase consists of continued testing and post-market monitoring. It’s also during this time that the FDA recommends a recall, if necessary.

Companies and Products Needing Coverage

The life sciences industry has a wide variety of companies offering products to the market. While each company has its unique business model and contribution, every leg of the process faces some exposure.

For example, during Phase 3, it’s standard to collect massive amounts of personal data from a patient testing pool. Protecting this sensitive information is the job of the life sciences company pursuing the FDA-approved status.

Along with patients’ data, consider intellectual property (IP insurance), patents, state-of-the-art testing equipment, employees, etc. Also, here are a few types of businesses who would benefit from having life sciences insurance coverage, too:

- Research and development companies

- Manufacturers

- Distributors

- Biological products companies

- Mainline brand developers (i.e., Pfitzer, Merck, Novartis, etc.)

- Generic competition companies

Understanding What Happens After Phase 3

Getting to Phase 3 is a feat in itself. Only five in every 5,000 compounds make it to this particular stage. And only one of those five will get approved by the FDA. So, it’s safe to say that the numbers are incredibly bleak. However, a few dark horses make it to the finish line.

If your new drug discovery is one of the fortunate, preceding through pre-clinical research and clinical trials, the FDA begins the fourth stage. This part of the process is typically the shortest, lasting only a few months.

In Phase 4, you’ll apply to market the drug. As you may have guessed, this application process is just as rigid as the rest of it. Some of the information contained in the application includes:

- Clinical results

- Labeling information

- Safety information

- Drug abuse potential

- Patient information

- Directions for use

After a meticulous 6-10 month scrutiny, the FDA conducts a comprehensive examination of the data, delving into the details. This exhaustive review culminates in a decisive verdict—either approval or disapproval. It’s routine for the FDA to seek additional information before reaching a conclusion, and occasionally, they identify issues that necessitate resolution before progressing in the process. Ensure the seamless journey of your pharmaceutical insurance and dietary supplement insurance through this meticulous regulatory procedure.

If you’re able to iron out all the wrinkles, the FDA review team greenlights the drug and works with you to develop information regarding prescribing. Even after releasing the drug on the market, problems with it still might surface, which is what Phase 5 addresses.

The last phase of the process focuses on post-market issues. Some developers want to change the drug formulation or have it approved for a different use, which the FDA must approve. While the drug is on the market — even after the patent expires — the FDA keeps a watchful eye on it.

Insurance Policies to Help Secure Success

While every life sciences company is different from the next, creating a kaleidoscope of unique risks to consider, here are a few foundational policies to help spur your success.

General liability insurance

We consider a general liability (GL) policy the firm foundation on which to build a robust commercial risk management plan. Without it, companies — life sciences companies included — can quickly shutter due to the fundamental risks of merely operating a business. That said, GL coverage works to protect life sciences companies against third-party lawsuits of bodily injury, property damage, personal injury, or advertising injury.

Property insurance

Besides a physical office, life sciences companies typically possess expensive and hard-to-replace equipment. Power outages, natural disasters, break-ins, etc. could be detrimental to your business, halting operations for days or weeks. Property insurance is an “indemnity” policy as opposed to a “liability” policy, which means it doesn’t require legal action to trigger it. If a covered physical loss occurs, your property insurance policy will respond.

Product liability insurance

Let’s be real, we live in a litigious society, and the bar for filing lawsuits is incredibly low nowadays. Although life sciences companies aspire to improve people’s lives and health, allegations are still tossed around in the industry. For example, you might be responsible for defense costs if a customer alleges that your product caused personal injury or property damage. Product liability insurance helps to cover situations, including manufacturing defects, design defects, and inadequate labeling.

D&O insurance

When VCs invest in your life sciences company, part of a typical deal is for the firm to place someone on your board of directors. With an ownership stake in the company, investors will want to guarantee that their employee is protected from legal liability. Directors and officers (D&O) coverage steps in to cover the VC. Also, if you and your investors dispute for any reason, they want to be assured that you have the financial safety net to absorb the defense fees without putting the future of the entire company at risk.

Cyber liability insurance

The further along a clinical trial progresses, the more significant your patient pool becomes. Not only does this involve more people in the process, but it opens up a door for data breaches — which can skyrocket to $4M on average. Cyber liability insurance can help to protect your company against third-party lawsuits arising from such a threat. Plus, cyber liability policies help cover fines and penalties from regulars, too.

Understanding the details of what coverage your life science company needs can be a confusing process. Founder Shield specializes in knowing the risks your industry faces to make sure you have adequate protection. Feel free to reach out to us, and we’ll walk you through the process of finding the right policy for you.

Want to know more about insurance for life sciences companies? Talk to us! You can contact us at info@foundershield.com or create an account here to get started on a quote.