Key Takeaways

Managing Partner; COO & Co-Founder

cAlthough robots aren’t “taking over the world,” as many sci-fi thrillers suggest, society depends on robotics now more than ever before. Several industries lean heavily on the use of robotics, too. These machines help to increase productivity, reduce risks to human beings, and improve product quality. The robotics industry has been extending its overall influence for many years. And yet, it’s challenging to keep up with the impact. In this post, we examine how the robot insurance world works, in particular, has been rocked by robotics.

Is Robotics Impacting Our Everyday Lives?

The short answer is yes — but people don’t always recognize how robotics influences daily life.

The use of robotics might come across as an untouchable and futuristic concept that only the Jetsons could manage. If you look around, though, there’s a good chance that you are more “Jetson” than you thought.

A decade ago, turning a house light on through voice activation was as farfetched as buying a flying car. Alexa and Siri are part of the universal family now. On wedding registries, for example, Millennials list smart speakers more frequently than cutlery or glassware nowadays. It’s only a matter of time before every individual has a robot to handle household chores. And that’s just for starters.

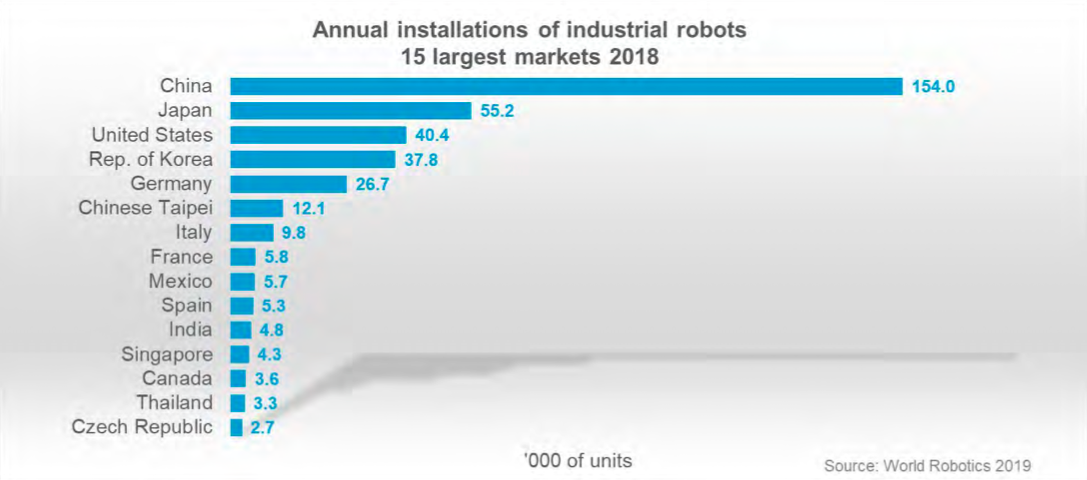

Robots are a significant part of manufacturing companies, working alongside their human counterparts daily. Only, most robots in factories are funny-looking arm extensions or massive emotionless machines as opposed to Will Smith’s bot army in the movie iRobot.

According to The Robot Report, the US has increased its robot installations for the eighth consecutive year, employing over 40,300 industrial robots. Check out the different rate countries are installing robots below.

How Do Robots Impact Insurance?

The use of robots in homes and industrial settings is happening at an alarming rate. What’s more, is that innovative changes and robotic upgrades also occur at lightning speed. Naturally, keeping up with these changes creates a challenging situation for insurance companies.

The primary question is, who is responsible if a robot goes rogue — the robot manufacturer, the homeowner, the manufacturing company? A malfunctioning or improperly programmed robot could quickly cause significant structural damage and injury or death to its human co-workers in a manufacturing setting.

The idea of “death by robot” became a reality in 1979 when the arm of a one-ton production line robot crushed Robert Williams. His family was awarded $10 million in damages because the court concluded that his death was the result of inadequate safety measures.

As we explore the benefits of integrating robotics into our daily lives, it’s essential to consider and manage the potential risks involved. In today’s modern homes, robots have taken on various tasks, such as vacuuming floors, managing household functions, and even fetching items for us. However, in the event that one of these robots goes rogue, it could lead to a range of issues similar to those seen in industrial settings, albeit on a smaller scale within our homes. These issues may manifest as scuffed flooring, damaged furniture, or even structural harm. It’s crucial to proactively address these risks to ensure a seamless and safe integration of robotics into our domestic spaces.

The insurance industry is having to navigate these ever-changing innovations in terms of what risks they pose. It’s no small feat.

What Coverage Is Important for Robotics?

The robotics industry faces several significant risks, including:

- Liability

- Human error

- Product failure

- Property loss

- Cybersecurity

As a result, insurance carriers transform their way of doing things to compensate for the rapid advancements and uncharted territory of robotics. Consider cybersecurity, for example, and the numerous vulnerabilities a robot possesses in humans attempting to program the machine. Cyber insurance must keep up with technological advancements, which can be challenging at times.

As mentioned, another valid concern is professional liability. Suppose a third party claims that a robotics company caused them financial loss, errors & omissions (E&O) insurance steps in to cover the legal costs. Complex litigation is a hassle to navigate, but robot insurance helps robotics companies to support innovation while protecting progress.

Robotics companies lean heavily on property insurance to provide coverage for damages to tangible property (i.e., high-end equipment, office space, etc.). This particular coverage reimburses companies that face real property being damaged or destroyed. As robots become more advanced and relied upon, property insurance will shift to accommodate the growing needs.

Cyber Risk Management Guide

How Do Underwriters Adapt to the Change?

Underwriters are notoriously tedious folks, combing through risk scenarios scrupulously. This leaving-no-stone-unturned approach requires a unique and thorough understanding of the actual threats robotics present to us humans. Only, the history of robotics, compared to other industries, is rather short-lived. So, drumming up solid stats is challenging.

Humans vs. robots

Firstly, underwriters examine the human-less aspect of using robotics. For example, unlike humans, robots don’t get tired, have bad days at work, or struggle with their emotions. Many of the reasons accidents happen in the home is because of human nature.

The absence of a limbic system provides more reliability in terms of accuracy. A robot won’t forget to turn off the stove or halt the production line because they’re ruminating over the words of a friend gone salty, per se. In theory, robots should deliver more stability to household functions. This reliability and security rely on the robot’s programmability, of course — which is the next topic under the microscope.

Startup and maintenance costs

Robots aren’t cheap. The price to replace parts and reprogram or repair them is something underwriters must take into account. On the one hand, startup and maintenance costs are a pretty penny. On the other hand, these costs are probably worth it because accidents and damages are less likely to occur with up-to-date and adequately functioning robots.

Other advantages

Lastly, underwriters look outside of the box for benefits robotics offer homeowners and industrial manufacturers alike. Robots typically have valuable sensors that could prevent other catastrophes from happening.

For example, consider a leaky pipe or malfunctioning temperature controls. Preventing high-dollar damage claims could offset the initial cost of robots, which is a price worth paying in the insurance world. Additionally, safeguarding intellectual property is crucial, as it protects the valuable innovations and technologies that these robots might incorporate.

Do Any New Development Influence Insurance?

New developments tend always to influence insurance. The latest growth is one more iron in the fire, one more player in the game…you get it.

The robotics industry rarely stands still. It’s a fluid market with evolving technology and plenty of fresh ideas to pursue. Insurance carriers have the tricky job of identifying what kind of technology honestly makes a difference in terms of risk. On the flip side, we also must pinpoint technology that will increase premiums.

Sometimes, new developments add cost to premiums because of the lack of historical references. In other words, underwriters without meaningful data are flying blind, depending mainly on guesswork. Only through secure analytics can insurance carriers categorize new developments accurately — which takes time.

How Do New Risks Affect Pricing?

In the insurance world, risks affect pricing more than most other variables. However, here are a few more factors that might affect premium cost:

- Coverage type

- Industry

- Claims history

- Risk management

- Structural setting

- Geography

Traditionally, insurers drive up premium costs parallel to the risk level. Or, at least, they try to accomplish this. Actuaries get the lucky job of balancing risk and cost in the insurance industry. It’s not uncommon to experience an uptick in premium costs when new threats arrive on the scene.

A robust risk management program can help to influence pricing — even in terms of the associated risks robotics face. A business employing robotics that is proactively addressing threats will likely experience better pricing.

Regarding robotics, both underwriters and actuaries have a tall order. Sophisticated algorithms (thanks to robotics) contribute to these complicated tasks, creating more ease and clarity in defining and rating risk.

As time progresses and robotics gain broader acceptance and understanding in industrial and residential settings, assessing risk should naturally become less intricate. In theory, with this increased familiarity, premium pricing should also decrease. This is particularly relevant for Broker Of Record (BOR), where enhanced understanding can contribute to a more streamlined risk evaluation and pricing structure.

Understanding the details of what coverage your company needs can be a confusing process. Founder Shield specializes in knowing the risks your industry faces to make sure you have adequate protection. Feel free to reach out to us, and we’ll walk you through the process of finding the right policy for you.