Carl Niedbala

Managing Partner; COO & Co-Founder

Key Takeaways

Managing Partner; COO & Co-Founder

Disclaimer: Please be advised that our brokerage is only authorized to provide commercial insurance coverage to Canadian companies that possess a legal business entity domiciled within the United States. Founder Shield can connect you with partners who can help establish a U.S. entity.

As in any industry, Canadian Service as a Software (Saas) companies face unique challenges. From data collection to outpatient management, SaaS companies offer an array of services. SaaS customers rely heavily on software products and services, needing them to be foolproof, stable, and fast — which is a tall order that insurance can help Canadian SaaS companies deliver.

Canadian SaaS Industry Overview

Although the SaaS business model is somewhat more complex than other structures, it’s cloud-based infrastructure attracts throngs of users. Customers pay a monthly subscription to gain access to the software operating through a web browser. Making SaaS products worthwhile requires some hefty coding and interface design skills.

The SaaS industry’s distinct approach has proven successful, especially in the world of startups. Over the past couple of years, investment in Canadian SaaS companies has skyrocketed. With over 445 active SaaS companies in Canada, most of them call Ontario their home base. Naturally, Ontario-based companies make up a significant chunk of all investment deals.

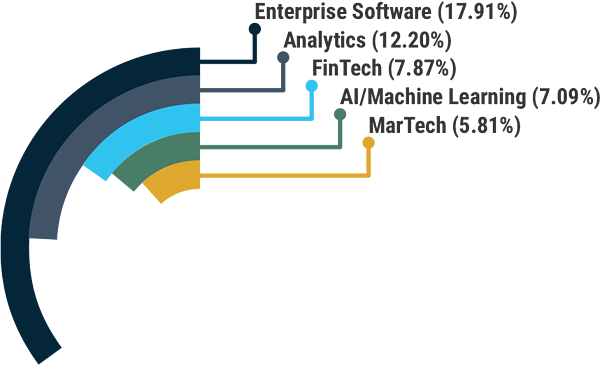

It’s safe to say that the Canadian SaaS industry isn’t going anywhere but up the charts. Consider the top five SaaS verticals — enterprise software, analytics, fintech, AI/machine learning, and martech — and their impact on the industry.

What Are the Risks for Canadian SaaS Companies?

As mentioned, every industry faces unique risks. However, Canadian SaaS companies must navigate plenty of technical challenges to ensure the industry endures.

Cybersecurity

With every data breach, cybercriminals are growing more sophisticated. These nameless villains no longer rely on elementary strategies to hack a system. Instead, cybercriminals execute sophisticated, multi-tiered attacks. Cyberattacks can quickly devastate small and mid-market companies and cause massive damage to global giants, as well.

It’s no surprise that the average cost of a data breach worldwide is $4 million — but that number jumps to $6.35 million for data breaches in Canada. Lamentably, this upward trend is nothing new for Canada. The good news is that Canada hasn’t turned a blind eye to these numbers and is proactive in protecting information security.

Since SaaS companies handle vast amounts of Personal Identifiable Information (PII), they have a lot at stake. This dynamic makes cybersecurity a top priority for Canadian SaaS companies.

Cyber Risk Management Guide

System Failures

According to IBM’s Cost of Data Breach Report 2020, malicious attacks caused 42% of Canadian breaches, system glitches caused 35%, and human error caused 23%. The stats tell us that cybersecurity should undoubtedly be a primary concern. But more importantly, these numbers point to human error as a significant risk SaaS companies face, too.

When humans are causing nearly a quarter of all data breaches, shutdowns, and software system failures, it’s a problem. SaaS customers depend heavily on the software to work safely, promptly, and efficiently. System failures, frequent or far between, could harm Canadian SaaS companies’ finances.

Loss of Recurring Revenue

Lastly, if navigating system failures and dodging cybercriminals wasn’t enough, SaaS companies also worry about recurring revenue loss. Let’s face it; when customers are dissatisfied with a platform or software, they’re going to shop around for something better.

This approach means customers will stop their recurring payments to a specific SaaS company and start paying a subscription fee to another one. As imagined, losing any amount of money is unhelpful, but losing a secure monthly cash flow is exceptionally harmful.

That said, the entire premise of SaaS income is based on recurring revenue or monthly fees in the form of subscriptions. Without this particular cash flow, Canadian SaaS companies could shutter. Naturally, SaaS companies do all they can to safeguard their business model of recurring revenue.

What Insurance Should Canadian SaaS Companies Purchase?

Each new risk in the SaaS industry presents an opportunity for SaaS insurance products to shine. Here are a handful of beneficial, must-have insurance policies to help ensure longevity for SaaS companies in Canada.

Errors and omissions (E&O) Insurance

Also known as professional liability insurance, E&O policies cover SaaS companies if an act, error, or omission occurs when the company delivers its professional services. Third-party lawsuits often arise after a disappointing service experience, mostly because these circumstances cause third-party financial harm. E&O insurance helps navigate complex litigation, responding to threats of professional service disputes.

Cyber liability insurance

When a data breach happens, SaaS companies could face mounds of lawsuits, plus fines and penalties from regulators. Notifying your customers is expensive enough, let alone monitoring credit, data restoration, and forensic analysis. Cyber liability insurance covers many direct expenses relating to a breach in cybersecurity.

Directors and officers (D&O) insurance

All companies, including Canadian SaaS companies, have key individuals who are responsible for managing the business. When allegations fly of breach of fiduciary duty or other claims relating to management, D&O insurance provides the capital to absorb legal costs without putting the SaaS company’s finances at risk.

Employment practices liability insurance (EPLI)

No matter the SaaS team’s size, having employees opens the door for common employment practices claims (i.e., harassment, discrimination, retaliation, and wrongful termination). EPLI coverage defends you and your organization, paying the judgment or settlement.

General liability (GL) insurance

Doing business in any industry results in facing several fundamental risks, such as the notorious “slip-and-fall” claims. However, when it comes to damaging a third party’s property or facing a products liability claim, a GL policy is what you want in your corner. Most SaaS companies consider GL insurance to be the foundation of protection to build a robust risk management plan.

Property insurance

On the one hand, plenty of Canadian SaaS companies rent their office space. On the other hand, owning property is popular, too. Property insurance protects your tangible property as well as the contents of the building itself. Consider the cost of replacing office supplies, high-end computer equipment, and cables after a weekend office fire or catastrophic storm.

With ruthless cyber criminals on the loose and customers depending on software daily, the best time for Canadian SaaS companies to protect themselves is now. Structuring your risk management plan with the right coverage is imperative. And working with a seasoned insurance professional is an excellent place to start.

Understanding the details of what coverage your SaaS company needs can be a confusing process. Founder Shield specializes in knowing the risks your industry faces to make sure you have adequate protection. Feel free to reach out to us, and we’ll walk you through the process of finding the right policy for you.

Disclaimer: Please be advised that our brokerage is only authorized to provide commercial insurance coverage to Canadian companies that possess a legal business entity domiciled within the United States. Founder Shield can connect you with partners who can help establish a U.S. entity.

Insurance Rebuilt, End-to-End